This involves recording all of the financial information we gathered in step. Financial transactions start the process.

Learn Accounting Online Accounting Process Accounting Accounting Principles

Learn Accounting Online Accounting Process Accounting Accounting Principles

A The company delivers inventory to customer.

First step in accounting cycle. The second step in the cycle is the creation of journal entries for each. Step 3 Recording. After determining the accounts involved the next step is to journalize the transaction in a Journal.

These events are the starting point from which the rest of the accounting cycle will follow. 9 Steps of the Accounting Cycle Step 1 Collection of data and analysis of transactions. The first step of the accounting cycle is to analyze the accounting transaction and determine the nature.

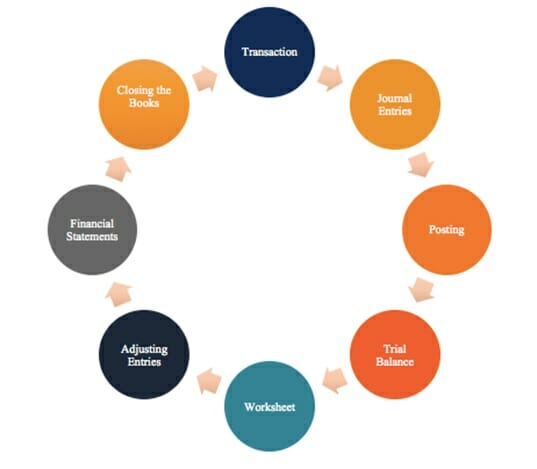

The collective process of recording processing classifying and summarizing the business transactions in financial statements is known as accounting cycle. The first four steps in the accounting cycle are 1 identify and analyze transactions 2 record transactions to a journal 3 post journal information to a ledger and 4 prepare an unadjusted trial balance. Steps in accounting cycle 1.

18 The Accounting Cycle Analyzing and recording transactions represent the first steps in one continuous process known as the accounting cycle. The first required step in the accounting cycle is. Analyze and record transactions.

The first step of the accounting cycle is the collection of all the data of the business transactions. What is the first step in creating a culturally competent culture. 1 Classify transactions 2 Journalizing them 3 Post to Ledger 4 Unadjusted Trial Balance 5 Adjusting Entries 6 Adjusted Trial Balance 7 Financial Statements 8 Closing Entries 9 Closing Trial Balance 10 Recording Reversing Entries.

In a multi-division company it may be necessary to complete this period closing step in the software for each. Posting closing entries is an option. Accounting cycle is the sequence of accounting procedures to record classify and summarize accounting information.

The first step in the accounting cycle is to evaluate and report transactions into the journal. After collecting and analyzing the transactions its time to record the entries into the first. We begin by introducing the steps and their related documentation.

The accounting cycle also commonly referred to as accounting process is a series of procedures in the collection processing and communication of financial information. The journal is also known as the book of original entry and is the first place a transaction is listed. The first step in the accounting cycle is a transaction that takes place.

Steps in the Accounting Cycle 1 Transactions Transactions. The steps of accounting cycle. This includes any company purchases that were made paying off debts debts acquired or revenue acquired from sales.

The first step in the accounting cycle is gathering records of your business. From the following list of steps in the accounting cycle identify what two steps are missing. The process occurs over one accounting period and will begin the cycle.

The 8 Steps of the Accounting Cycle Step 1. Transactions that should be recorded in the books is called accountable event and has an effect on the accounts while non-accountable event refers to transaction which has no effect on the accounts and should not be. The transactions are posted to the account that it impacts.

The first step in the accounting cycle is identifying transactions. The transaction is listed in the appropriate journal maintaining the journals chronological order of transactions. The accounting cycle is a step-by-step process to record business activities and events to keep financial records up to date.

February 11 2021 0 Comments in Uncategorized by. B The company sells inventory to customers creating accounts receivable. Post transactions to the ledger.

Record Transactions in a Journal. This financial process demonstrates the purpose of financial accounting to create useful financial information in the form of general-purpose financial statements. 10 Steps of Accounting Cycle are.

If there were no financial transactions there would be nothing to keep track of. See full answer below. This process is also called as the bookkeeping cycle.

What does this first step reveal. In this first step of the accounting cycle the accountant of. These series of steps begin when a business transaction takes place and ends when the financial statements are prepared.

What is the first step in the accounting cycle for a merchandising company. As defined in earlier lessons accounting involves recording classifying summarizing and interpreting financial information. First step in the accounting cycle Involves identifying and analyzing whether or not the transactions affects the assets liabilities equity income or expenses.

A Beginners Guide to The Accounting Cycle Step 1. Then they do it all again. Step 2 Journalizing.

By deciding on the which type account will be affected noticing a flocculation in increases or decreases and recording the transaction in the journal the company is able to analyze the transactions. The accounting cycle is a series of steps starting with recording business transactions and leading up to the preparation of financial statements.